Simple to set up. Powerful over time. Designed to last beyond traditional retirement plans.

Savvly is easy to set up and simple to manage. Employers choose to offer Savvly as a standalone benefit or alongside existing retirement plans like 401(k)s.

Employees receive monthly contributions that grow over time.

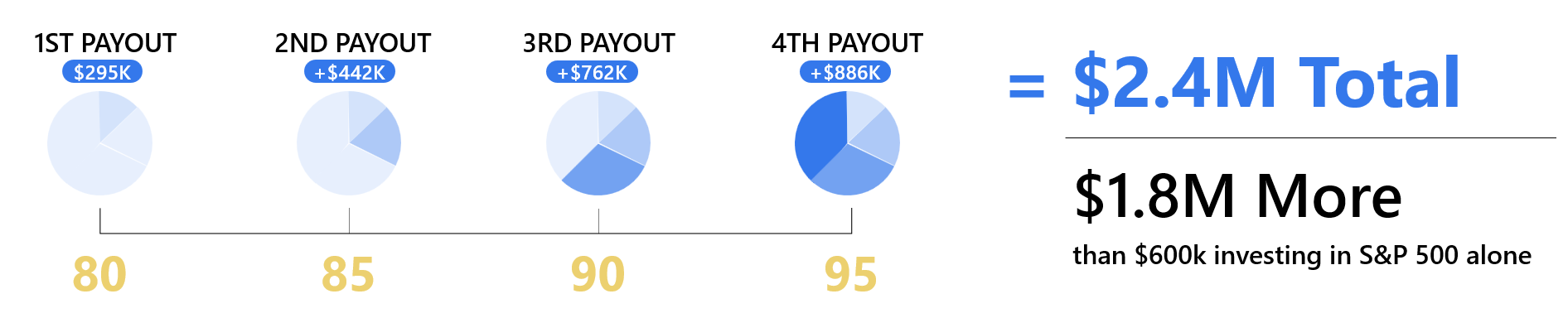

When employees reach age 80, Savvly may begin to provide monthly income.

Note: the average long-term S&P 500 return has been 9%. The outcome shown above is an estimate of the sum of the four payouts at 80, 85, 90 and 95. The amount of these payouts depend on the return of the S&P 500 and the performance of the pension pool. See assumptions and disclosures at www.savvly.com/employers

This longevity benefit is designed to kick in after other benefits (like 401(k)s or Social Security) may run low.

Income can begin at 80 and continue through the rest of life.

Amounts depend on years of participation, total contributions, and account growth.

.png)

No, the Longevity Benefit isn’t insurance, it’s built on a low-cost S&P 500 index fund and distributes more proceeds to investors who live longer.

Yes! It’s a new longevity benefit offered for your financial well-being. (Check with your employer for details)

No, the Longevity benefit is not a traditional investment fund. It's a Longevity Benefit where your assets are invested in low cost S&P 500 ETFs, held and protected by a third-party custodian. Savvly Advisor LLC manages the process of new investors entering and exiting the fund.

As a qualified ROTH account. You should consult with a tax advisor. Savvly does not provide tax advice.

Unlike some traditional pensions, your family or estate receives all, or the vast majority, of your deposits back. (Please refer to the disclosure for details.)

You keep your account, and you can continue funding it, but your company will stop paying into it.

Savvly is a modern benefit that supports your workforce, today and tomorrow. Add it as a standalone option or supplement existing plans like 401ks.