%20(1).png)

%20(1).png)

Deciding when to retire is one of the most significant and personal decisions you'll make in your lifetime. It's not just about choosing an age but considering a range of factors that can impact your financial security, lifestyle, and overall well-being.

To help you navigate this important decision, let's explore the key elements to consider: financial readiness, health, personal goals, and lifestyle preferences.

Originally published: May 31, 2024

Your financial situation is a critical factor in determining when to retire. Here are some key points to consider:

Your health also plays a crucial role in deciding when to retire. Consider the following:

Retirement is an opportunity to pursue personal goals and interests. Think about:

Your desired lifestyle in retirement will also impact your decision:

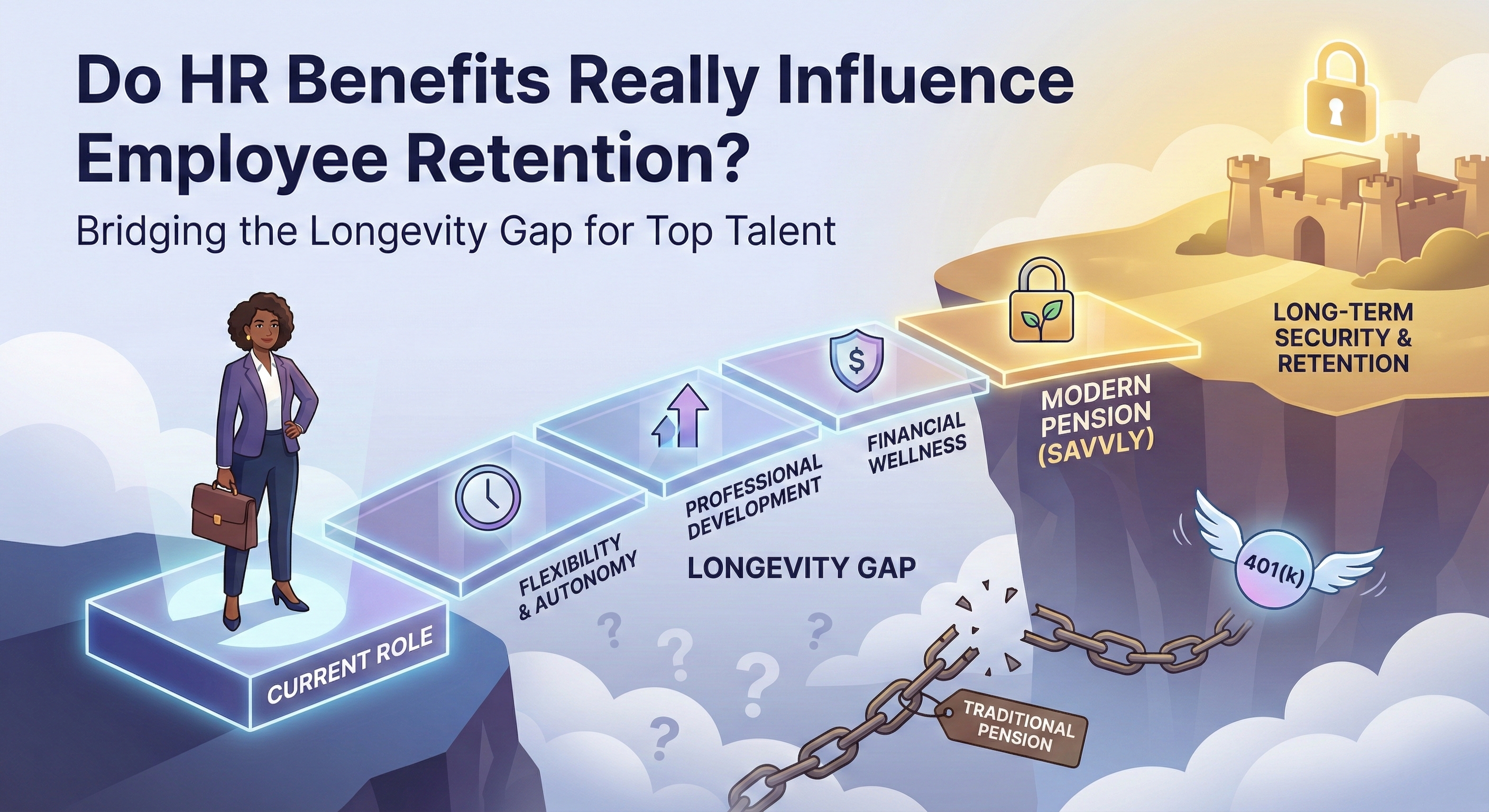

The Savvly Longevity Benefit is designed to deliver scheduled income at later-life milestones for investors who reach them. It adds a longevity-based reallocation layer to market-linked performance, adding scheduled payouts at ages 80, 85, 90, and 95 for investors who reach those milestones. Savvly is not insurance and not FDIC insured; payout amounts are not guaranteed. Learn more at savvly.com/disclosures.

Deciding when to retire is a multifaceted decision that requires careful consideration of your financial readiness, health, personal goals, and lifestyle preferences. There's no one-size-fits-all answer, as everyone's situation is unique.

Take the time to evaluate your circumstances, consult with a financial advisor if needed, and make a plan that aligns with your vision for a fulfilling retirement. Whether you choose to retire early, at the traditional age, or even later, the key is to ensure that your decision supports a happy, healthy, and financially secure future.

The 25x rule is a planning benchmark that suggests accumulating 25 times your expected annual retirement expenses before retiring. This figure is based on the 4% withdrawal guideline, introduced in research by financial planner William Bengen published in the Journal of Financial Planning. That research found that retirees could withdraw 4% of a balanced portfolio annually over a 30-year period without depleting it in most historical market scenarios. Individual results depend on actual expenses, investment returns, and how long the retirement period lasts.

Financial readiness for retirement typically includes having sufficient savings to cover expected expenses throughout the retirement period, a plan for healthcare coverage, a strategy for Social Security timing, and an accounting of all income sources including pensions, investment accounts, and part-time income. The Social Security Administration (SSA) provides benefit estimates and retirement planning tools at ssa.gov/myaccount.

Medicare eligibility begins at age 65. Those who retire before 65 are responsible for arranging private health coverage during the gap period. Options include COBRA continuation coverage (available for up to 18 months after leaving employer coverage), Affordable Care Act marketplace plans, and coverage through a spouse's employer. Medicare.gov and HealthCare.gov provide details on coverage options for early retirees.

Social Security retirement benefits can be claimed as early as age 62 or as late as age 70. Claiming before full retirement age, which ranges from 66 to 67 depending on birth year, results in permanently reduced monthly payments. Claiming after full retirement age earns delayed retirement credits of 8% per year up to age 70, permanently increasing the monthly payment. The Social Security Administration publishes a chart showing how age at claiming affects benefit amounts.

This article is for informational purposes only and does not constitute financial, tax, or investment advice. Consult a qualified financial professional before making retirement planning decisions.

Disclosures

The information on this page is provided for educational purposes only and is not intended as investment, legal, or tax advice. It is designed solely to illustrate how longevity-linked investment benefits may work under certain assumptions. Actual results will vary. All illustrations, examples, and case studies are hypothetical and are intended to demonstrate potential scenarios — not to predict or guarantee actual outcomes. They do not represent the performance of any individual investor, portfolio, or account.

Key Assumptions Used in the Illustrations

Life expectancy and mortality projections are based on the most recent Social Security Administration (SSA) tables available at the time of simulation.

In the event of death or early withdrawal, hypothetical scenarios assume that investors who exit early, or their estate in the event of death, may receive 75% of the lesser of the initial investment or current market value, plus 1% for each full year the account was active. Case studies assume standardized market growth of 8% annually and do not incorporate unexpected market volatility, inflation, changes in interest rates, or changes in an investor's personal circumstances.

Simulations may assume a 3% annual early withdrawal rate prior to payout or death. All figures shown are net of fees. No forecast, projection, or hypothetical return should be relied upon as a promise or representation of future performance.

Past performance is not indicative of future results. The 8% annual market growth rate used in illustrations is a standardized assumption for modeling purposes only and does not represent the historical or expected performance of any specific investment. Note that early or voluntary withdrawals by other participants can affect fund performance and the size of distributions, and that a higher-than-expected number of participants reaching payout milestones may reduce the per-participant benefit received.

Savvly's Longevity Benefit is not a bank product, not FDIC insured, not insured by any federal government agency, and not insurance; payout amounts are not guaranteed. Investment values may decline..

Savvly's Longevity Benefit may not be suitable for all investors. Eligibility to invest is subject to qualification requirements and not all investors will be eligible. Investors should carefully consider their investment objectives, risk tolerance, time horizon, and financial situation before investing. See savvly.com/disclosures for current eligibility criteria, fees, risks, withdrawal terms, and fund assumptions.

This content is published by Savvly, Inc. Savvly has a financial interest in the products described and this content should not be interpreted as independent financial research or analysis. Investors should carefully evaluate their own circumstances and consult a qualified financial professional before making any investment decision.

.png)