%20(1).png)

%20(1).png)

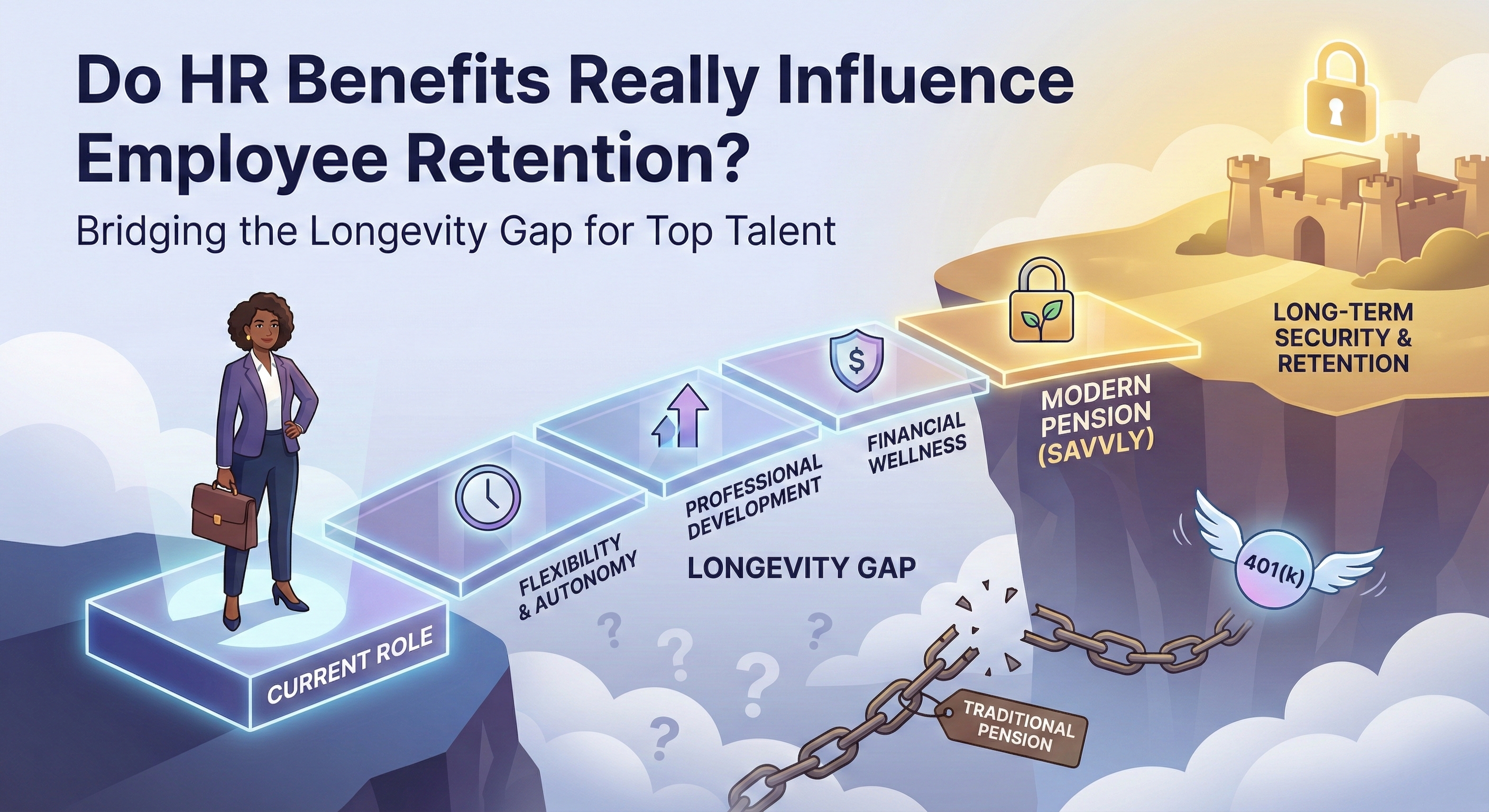

The transition from defined benefit pensions to defined contribution plans like 401(k)s has fundamentally changed the retirement landscape. While these changes have provided some benefits, they have also exposed significant shortcomings in the current system, leaving many Americans unprepared for retirement.

Originally published: September 19, 2024

One of the primary issues with 401(k) plans is that they place the responsibility of saving and investing squarely on the individual. Workers may lack the financial literacy required to make informed investment decisions, leading to suboptimal retirement savings outcomes. Additionally, market volatility can significantly impact the value of 401(k) accounts, especially for those nearing retirement who may not have the time to recover from market downturns.

Studies have shown that a significant portion of the American workforce is not saving enough for retirement. According to a report by the National Institute on Retirement Security, nearly 40% of working-age Americans have no retirement savings at all. Those who do save often contribute insufficient amounts, partly due to economic pressures such as stagnant wages, high cost of living, and mounting debt. The median retirement account balance for Americans nearing retirement is alarmingly low, indicating a looming crisis.

Another critical issue is the decline in employer contributions to retirement plans. While some employers match a portion of employee contributions to 401(k)s, these matches are often less generous than the benefits provided by traditional pensions. This reduction in employer support places an even greater burden on individuals to fund their own retirements.

Increasing life expectancy is another challenge. People are living longer, which means their retirement savings need to last longer. Coupled with rising healthcare costs, this could create additional financial strain on retirees. Many find their savings insufficient to cover expenses throughout their retirement years, which can lead to a lower standard of living.

Given these challenges, it is clear that the current retirement system is not adequate for ensuring financial security for all retirees. A new solution is needed – one that combines the strengths of both defined benefit and defined contribution plans while addressing their respective weaknesses.

One potential approach is the introduction of hybrid retirement plans that incorporate elements of both DB and DC plans. These plans could provide a guaranteed base level of income, supplemented by individual contributions and investment growth. Another approach is to expand access to retirement savings programs through policy changes, such as automatic enrollment in retirement plans and increased incentives for both individuals and employers to save.

Improving financial literacy is also crucial. Providing education and resources to help individuals understand and manage their retirement savings can lead to better outcomes. Employers, government agencies, and financial institutions all have a role to play in promoting financial literacy.

Savvly’s Longevity Benefit is designed to help investors build potential income for the later years of retirement. It adds a longevity-based reallocation layer to market-linked performance, creating the opportunity for additional payouts at ages 80, 85, 90, and 95 for investors who reach those milestones. Savvly is not insurance, not a guaranteed product, and not FDIC insured. For full details on fees, assumptions, risks, eligibility, and disclosures, visit savvly.com/disclosures.

The current retirement system, dominated by 401(k) plans, has significant limitations that leave many Americans vulnerable. A comprehensive, multi-faceted approach is needed to address these issues and ensure that all workers can achieve a secure and dignified retirement. By combining innovative retirement plan designs, supportive policies, and enhanced financial literacy, we can build a more robust and equitable retirement system for the future.

This article is for informational purposes only and does not constitute financial, tax, or investment advice. Consult a qualified financial professional before making retirement planning decisions.

Disclosures

The information on this page is provided for educational purposes only and is not intended as investment, legal, or tax advice. It is designed solely to illustrate how longevity-linked investment benefits may work under certain assumptions. Actual results will vary. All illustrations, examples, and case studies are hypothetical and are intended to demonstrate potential scenarios — not to predict or guarantee actual outcomes. They do not represent the performance of any individual investor, portfolio, or account.

Key Assumptions Used in the Illustrations

Life expectancy and mortality projections are based on the most recent Social Security Administration (SSA) tables available at the time of simulation.

In the event of death or early withdrawal, hypothetical scenarios assume that investors who exit early, or their estate in the event of death, may receive 75% of the lesser of the initial investment or current market value, plus 1% for each full year the account was active. Case studies assume standardized market growth of 8% annually and do not incorporate unexpected market volatility, inflation, changes in interest rates, or changes in an investor's personal circumstances.

Simulations may assume a 3% annual early withdrawal rate prior to payout or death. All figures shown are net of fees. No forecast, projection, or hypothetical return should be relied upon as a promise or representation of future performance.

Past performance is not indicative of future results. The 8% annual market growth rate used in illustrations is a standardized assumption for modeling purposes only and does not represent the historical or expected performance of any specific investment. Note that early or voluntary withdrawals by other participants can affect fund performance and the size of distributions, and that a higher-than-expected number of participants reaching payout milestones may reduce the per-participant benefit received.

Savvly's Longevity Benefit is not a bank product, not FDIC insured, not insured by any federal government agency, not a guaranteed or insured investment, and not insurance. Investment values may decline.

Savvly's Longevity Benefit may not be suitable for all investors. Eligibility to invest is subject to qualification requirements and not all investors will be eligible. Investors should carefully consider their investment objectives, risk tolerance, time horizon, and financial situation before investing. See savvly.com/disclosures for current eligibility criteria, fees, risks, withdrawal terms, and fund assumptions.

This content is published by Savvly, Inc. Savvly has a financial interest in the products described and this content should not be interpreted as independent financial research or analysis. Investors should carefully evaluate their own circumstances and consult a qualified financial professional before making any investment decision.

.png)