%20(1).png)

%20(1).png)

Originally published: February 9, 2026

The war for high-impact talent, the innovators, the leaders, and the technical experts who drive your bottom line, is more intense than ever.

When a "B-player" leaves, it's a disruption. When an "A-player" walks out the door, it's a catastrophe. Research from Gallup and the Society for Human Resource Management (SHRM) suggests that replacing a specialized or senior employee can cost an organization up to 2x that employee's annual salary when you account for recruiting, onboarding, lost institutional knowledge, and the "productivity vacuum" left behind.

As compensation costs skyrocket, HR leaders are facing a critical strategic pivot: Are your benefits actually protecting your most valuable human capital, or are you just funding your competitors' next great hires?

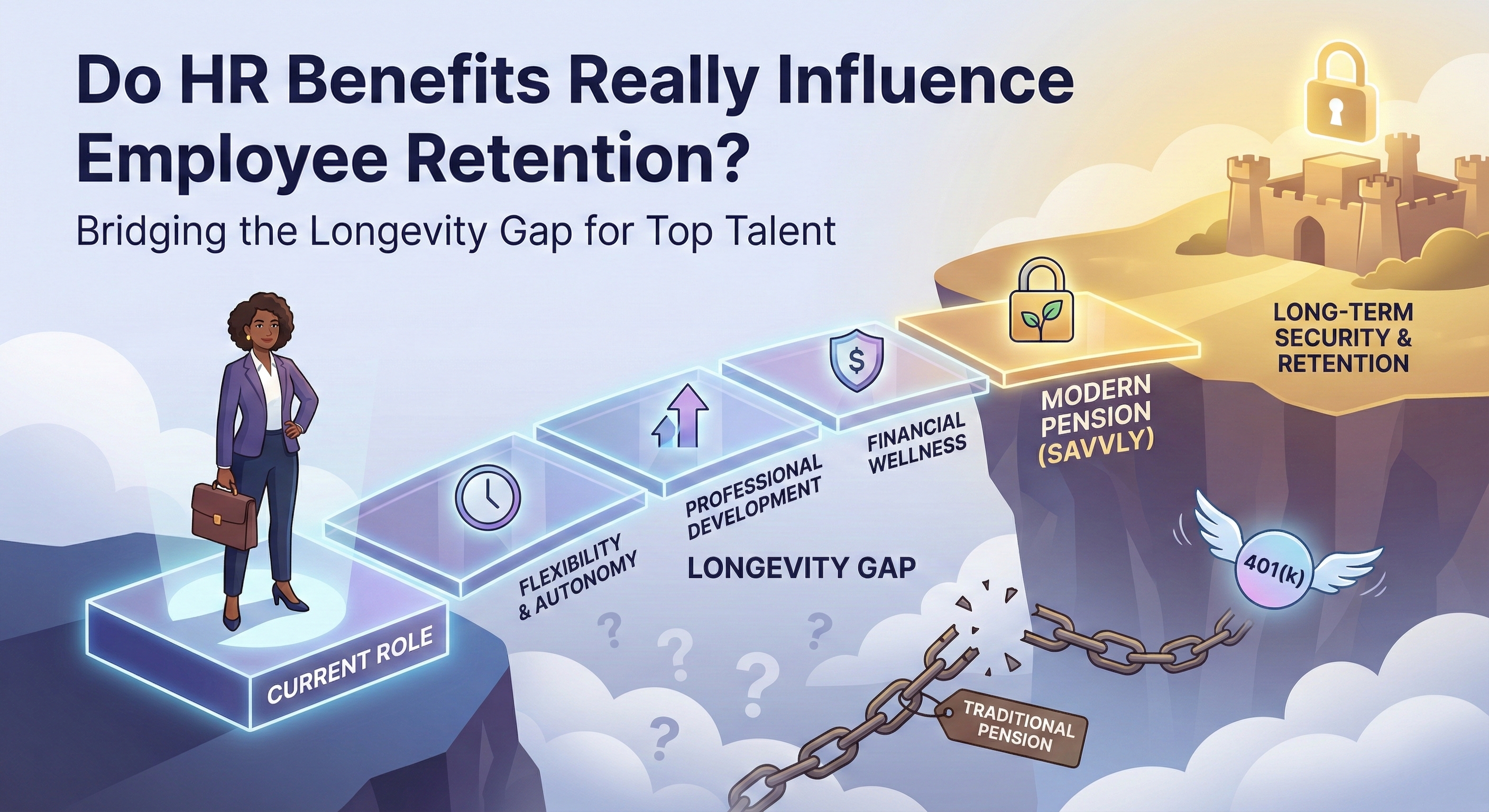

The idea that pensions are the only benefit that significantly locks in employees has some basis in reality. The most enduring example of "benefit-driven retention" is in the public sector. Why do government roles, which often offer lower base salaries than the private sector, boast such high retention for key talent? The secret is the Defined Benefit Pension.

Data from the National Institute on Retirement Security shows that 90% of workers with a pension say it makes them more likely to stay in their job. In these environments, the "golden handcuff" isn't a myth; it's a mathematical reality. But in the private sector, where pensions have vanished, we've traded that long-term security for the flexibility of the 401(k). In doing so, we may have accidentally incentivized job-hopping.

If you don't have a traditional pension, what levers can you pull to keep your best people? According to the MetLife Employee Benefit Trends Study, employees who are satisfied with their benefits report significantly higher loyalty to their employer.

Key benefits shown to move the needle include:

Employees today value portability. They love the 401(k) and the Health Savings Account (HSA) because they "own" them. However, for the employer, portability has a downside: it doesn't create a reason to stay.

A 401(k) is a wealth-accumulation tool, but it doesn't solve "longevity anxiety," the fear of outliving one's money. Your best employees are often the most financially literate; they know that a market downturn at age 70 could wipe out their security. To influence true loyalty, you need a benefit that offers the security of a pension with the modernity of a defined contribution.

The most innovative CHROs and Benefits managers are realizing they don't need the massive liabilities of a 1950s pension plan to get "pension-like" retention. Instead, they are looking at Longevity Benefits.

Savvly is designed to complement the 401(k) by adding a longevity layer. While a 401(k) funds the first 20 years of retirement, Savvly adds scheduled payouts at ages 80, 85, 90, and 95 to help replenish savings for employees who reach those milestones.

The Savvly Longevity Benefit is designed to deliver scheduled income at later-life milestones for investors who reach them. It adds a longevity-based reallocation layer to market-linked performance, adding scheduled payouts at ages 80, 85, 90, and 95 for investors who reach those milestones. Savvly is not insurance and not FDIC insured; payout amounts are not guaranteed. For full details on fees, assumptions, risks, eligibility, and disclosures, visit savvly.com/disclosures.

Does cash matter? Of course. Competitive cash compensation gets you in the game; a strong total rewards package wins it. The Willis Towers Watson Global Benefits Attitudes Survey found that while base pay is the top reason employees join a company, retirement security is consistently cited among the top reasons they stay. If you only compete on cash, you will always lose your best people to the next highest bidder. If you compete on security and longevity, you build a moat around your talent.

Replacing your best talent is a cost you can't afford. In a world where everyone is fighting for the same skilled workers, the company that solves the "Longevity Gap" will be the one that keeps its leaders.

By complementing the portability of the 401(k) with the late-life income potential Savvly can add, you create a modern version of the "government pension" effect: giving your best employees a reason to stay that a slightly higher salary elsewhere simply cannot match.

To learn how Savvly can complement your benefits strategy, visit savvly.com/contact-us.

This article is for informational purposes only and does not constitute financial, tax, or investment advice. Consult a qualified financial professional before making retirement planning decisions.

Disclosures

The information on this page is provided for educational purposes only and is not intended as investment, legal, or tax advice. It is designed solely to illustrate how longevity-linked investment benefits may work under certain assumptions. Actual results will vary. All illustrations, examples, and case studies are hypothetical and are intended to demonstrate potential scenarios — not to predict or guarantee actual outcomes. They do not represent the performance of any individual investor, portfolio, or account.

Key Assumptions Used in the Illustrations

Life expectancy and mortality projections are based on the most recent Social Security Administration (SSA) tables available at the time of simulation.

In the event of death or early withdrawal, hypothetical scenarios assume that investors who exit early, or their estate in the event of death, may receive 75% of the lesser of the initial investment or current market value, plus 1% for each full year the account was active. Case studies assume standardized market growth of 8% annually and do not incorporate unexpected market volatility, inflation, changes in interest rates, or changes in an investor's personal circumstances.

Simulations may assume a 3% annual early withdrawal rate prior to payout or death. All figures shown are net of fees. No forecast, projection, or hypothetical return should be relied upon as a promise or representation of future performance.

Past performance is not indicative of future results. The 8% annual market growth rate used in illustrations is a standardized assumption for modeling purposes only and does not represent the historical or expected performance of any specific investment. Note that early or voluntary withdrawals by other participants can affect fund performance and the size of distributions, and that a higher-than-expected number of participants reaching payout milestones may reduce the per-participant benefit received.

Savvly's Longevity Benefit is not a bank product, not FDIC insured, not insured by any federal government agency, and not insurance; payout amounts are not guaranteed. Investment values may decline..

Savvly's Longevity Benefit may not be suitable for all investors. Eligibility to invest is subject to qualification requirements and not all investors will be eligible. Investors should carefully consider their investment objectives, risk tolerance, time horizon, and financial situation before investing. See savvly.com/disclosures for current eligibility criteria, fees, risks, withdrawal terms, and fund assumptions.

This content is published by Savvly, Inc. Savvly has a financial interest in the products described and this content should not be interpreted as independent financial research or analysis. Investors should carefully evaluate their own circumstances and consult a qualified financial professional before making any investment decision.

.png)