%20(1).png)

%20(1).png)

Originally published: February 6, 2025

Changing jobs is a wonderful opportunity to start fresh and go to the next step in your career. But when you turn the page and move on to new opportunities, you face some loose ends to tie up – especially with your retirement accounts.

Many job-switchers overlook 401(k) management. Specifically, what should you do with your old 401(k)?

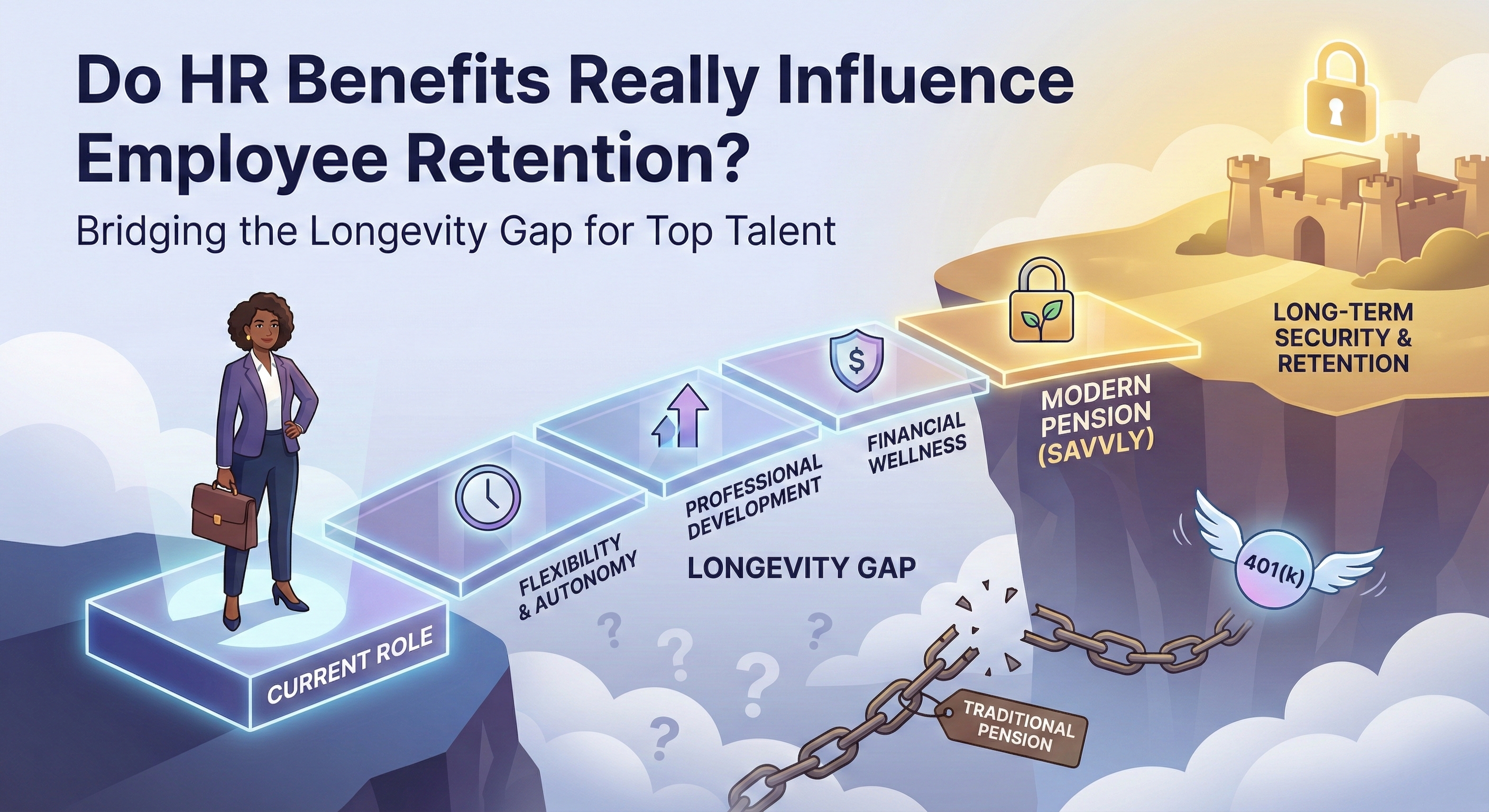

According to the Bureau of Labor Statistics, the average American holds nearly 13 jobs between ages 18 and 58.

That's potentially 13 old 401(k) accounts left behind! An estimated 31.9 million forgotten 401(k)s exist, with over $2.1 trillion in assets sitting untouched.

With so much money at stake, you need to keep your retirement savings from getting lost in the shuffle when you change jobs. So today, let's explore what your options are for your 401(k) when you change jobs.

Here are the four main choices you have to manage your 401(k) when you get a new job:

This move neatly consolidates your savings into one place, giving you more control and simplicity. But before transferring your 401(k), compare fees, investment choices, and other key details in both plans. You want assurance your money will keep working as hard for you in the new account.

Converting your traditional 401(k) to a Roth IRA is like giving your retirement savings a healthy upgrade. Yes, you'll pay taxes upfront. But as an educated investor knows, future tax-free withdrawals make this move worthwhile. Converting makes particular sense if you expect to land in a higher tax bracket down the road.

Sometimes, the best move is no move at all. Leaving it in place may be ideal if your old 401(k) has great investment options and low fees. Just remember you can no longer contribute, so you must track it separately from new accounts. There is no "out of sight, out of mind" here.

Seeing that lump-sum payout can be tempting. But cashing out your 401(k) early is like eating all your retirement savings at once. It may satisfy short-term cravings, but you'll regret it later. Cashing out before 59 1/2 leads to taxes, penalties, and lost growth. Only consider this nuclear option in true financial emergencies.

Managing your 401(k) during job changes isn't just about being savvy. Here are three key reasons it matters:

Take charge when you switch jobs and ensure you're making informed decisions. Your future self will thank you.

When someone leaves a job, the vested 401(k) balance stays in the account until the account owner takes action. Most plans allow former employees to keep the account invested with the same provider. Some plans begin mandatory distribution procedures for small balances below a plan-specific threshold. According to research by Capitalize, an estimated 31.9 million forgotten 401(k) accounts hold approximately $2.1 trillion in assets.

There are four primary options for a 401(k) from a previous employer: leave it in the former employer's plan if the plan allows; roll it into the new employer's 401(k) plan; roll it into an individual retirement account (IRA); or take a cash distribution. A cash distribution is subject to ordinary income tax and, for account owners under age 59.5, a 10% early withdrawal penalty. The IRS provides rollover guidance at IRS.gov.

Withdrawals from a traditional 401(k) before age 59.5 are generally subject to ordinary income tax plus a 10% early withdrawal penalty. Certain exceptions apply, including separation from service at age 55 or older for that employer's plan, substantially equal periodic payments, and specific hardship provisions. The IRS maintains a list of exceptions at IRS.gov.

A Roth conversion involves moving funds from a traditional 401(k) or traditional IRA into a Roth IRA. The converted amount is included in gross income in the year of conversion and is subject to ordinary income tax at that time. After conversion, funds in the Roth IRA grow tax-free and qualified withdrawals in retirement are not taxed. The IRS explains Roth conversion rules at IRS.gov.

This article is for informational purposes only and does not constitute financial, tax, or investment advice. Consult a qualified financial professional before making retirement planning decisions.

Disclosures

The information on this page is provided for educational purposes only and is not intended as investment, legal, or tax advice. It is designed solely to illustrate how longevity-linked investment benefits may work under certain assumptions. Actual results will vary. All illustrations, examples, and case studies are hypothetical and are intended to demonstrate potential scenarios — not to predict or guarantee actual outcomes. They do not represent the performance of any individual investor, portfolio, or account.

Key Assumptions Used in the Illustrations

Life expectancy and mortality projections are based on the most recent Social Security Administration (SSA) tables available at the time of simulation.

In the event of death or early withdrawal, hypothetical scenarios assume that investors who exit early, or their estate in the event of death, may receive 75% of the lesser of the initial investment or current market value, plus 1% for each full year the account was active. Case studies assume standardized market growth of 8% annually and do not incorporate unexpected market volatility, inflation, changes in interest rates, or changes in an investor's personal circumstances.

Simulations may assume a 3% annual early withdrawal rate prior to payout or death. All figures shown are net of fees. No forecast, projection, or hypothetical return should be relied upon as a promise or representation of future performance.

Past performance is not indicative of future results. The 8% annual market growth rate used in illustrations is a standardized assumption for modeling purposes only and does not represent the historical or expected performance of any specific investment. Note that early or voluntary withdrawals by other participants can affect fund performance and the size of distributions, and that a higher-than-expected number of participants reaching payout milestones may reduce the per-participant benefit received.

Savvly's Longevity Benefit is not a bank product, not FDIC insured, not insured by any federal government agency, and not insurance; payout amounts are not guaranteed. Investment values may decline..

Savvly's Longevity Benefit may not be suitable for all investors. Eligibility to invest is subject to qualification requirements and not all investors will be eligible. Investors should carefully consider their investment objectives, risk tolerance, time horizon, and financial situation before investing. See savvly.com/disclosures for current eligibility criteria, fees, risks, withdrawal terms, and fund assumptions.

This content is published by Savvly, Inc. Savvly has a financial interest in the products described and this content should not be interpreted as independent financial research or analysis. Investors should carefully evaluate their own circumstances and consult a qualified financial professional before making any investment decision.

.png)