%20(1).png)

%20(1).png)

Once you hit your forties, retirement looms ahead like a coveted prize. But that doesn't mean you have to relegate easing off work to your late fifties or early sixties. Phased retirement provides that bridge between a full work week and the more relaxed retirement days. You get to ease your foot off full-tilt work schedules and slide into something that allows you to enjoy the benefits of retirement well before the proverbial golden handshake.

Originally published: October 2, 2024

And you're not alone, as many as 47% of Americans think of retirement as a slow transition away from work. During phased retirement, you gradually reduce your working hours until you reach full retirement. This can happen as early as in your forties, or even once you've passed regular retirement age.

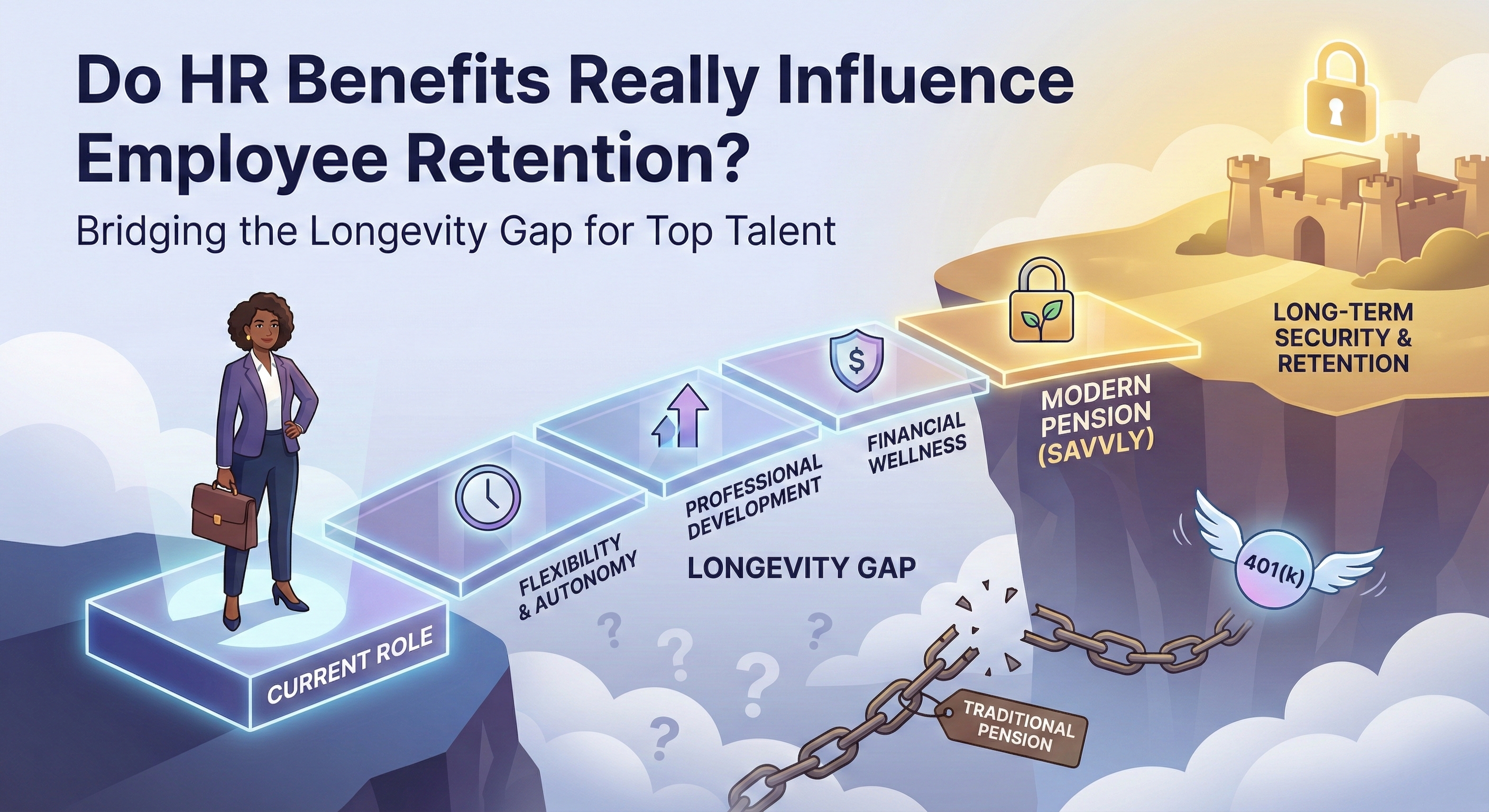

There are many reasons to consider phased retirement, such as:

To get the most out of a phased retirement, ensure a smooth transition. These tips might ease you on the way:

Whether you choose to stay part-time in your current role or you're broadening your horizons to freelance or do contract work for someone else, it's important to hand over the reins to someone else. Choose a successor and work through their roles and responsibilities. Set the person up in a way that would ensure a smooth transition.

Work through your personal budget, retirement benefits, and other financial considerations before retiring. Work with your financial advisor to pinpoint holes in your budget and possible solutions.

Phased retirement means that you still have to focus on work, even if it's just a few days a week. A schedule will help you allocate days for work and days for leisure, which prevents overcommitment and the possibility of phasing back into a full work cycle.

Work/life balance includes spending time with your loved ones. Make time for social engagements such as a round of golf or dinner with friends.

An attorney can help you work through your work contracts and benefits to determine how phased retirement might affect things such as vacation days, health care, profit share, and bonuses.

You can approach your existing employer to reduce your work hours. You can also look at other options such as contracting and freelance work.

A phased transition takes planning: financial, legal, and personal. Working with a qualified advisor before making changes to your schedule or benefits is a smart first step.

The Savvly Longevity Benefit is designed to deliver scheduled income at later-life milestones for investors who reach them. It adds a longevity-based reallocation layer to market-linked performance, adding scheduled payouts at ages 80, 85, 90, and 95 for investors who reach those milestones. Savvly is not insurance and not FDIC insured; payout amounts are not guaranteed. Learn more at savvly.com/disclosures.

This article is for informational purposes only and does not constitute financial, tax, or investment advice. Consult a qualified financial professional before making retirement planning decisions.

Disclosures

The information on this page is provided for educational purposes only and is not intended as investment, legal, or tax advice. It is designed solely to illustrate how longevity-linked investment benefits may work under certain assumptions. Actual results will vary. All illustrations, examples, and case studies are hypothetical and are intended to demonstrate potential scenarios — not to predict or guarantee actual outcomes. They do not represent the performance of any individual investor, portfolio, or account.

Key Assumptions Used in the Illustrations

Life expectancy and mortality projections are based on the most recent Social Security Administration (SSA) tables available at the time of simulation.

In the event of death or early withdrawal, hypothetical scenarios assume that investors who exit early, or their estate in the event of death, may receive 75% of the lesser of the initial investment or current market value, plus 1% for each full year the account was active. Case studies assume standardized market growth of 8% annually and do not incorporate unexpected market volatility, inflation, changes in interest rates, or changes in an investor's personal circumstances.

Simulations may assume a 3% annual early withdrawal rate prior to payout or death. All figures shown are net of fees. No forecast, projection, or hypothetical return should be relied upon as a promise or representation of future performance.

Past performance is not indicative of future results. The 8% annual market growth rate used in illustrations is a standardized assumption for modeling purposes only and does not represent the historical or expected performance of any specific investment. Note that early or voluntary withdrawals by other participants can affect fund performance and the size of distributions, and that a higher-than-expected number of participants reaching payout milestones may reduce the per-participant benefit received.

Savvly's Longevity Benefit is not a bank product, not FDIC insured, not insured by any federal government agency, and not insurance; payout amounts are not guaranteed. Investment values may decline..

Savvly's Longevity Benefit may not be suitable for all investors. Eligibility to invest is subject to qualification requirements and not all investors will be eligible. Investors should carefully consider their investment objectives, risk tolerance, time horizon, and financial situation before investing. See savvly.com/disclosures for current eligibility criteria, fees, risks, withdrawal terms, and fund assumptions.

This content is published by Savvly, Inc. Savvly has a financial interest in the products described and this content should not be interpreted as independent financial research or analysis. Investors should carefully evaluate their own circumstances and consult a qualified financial professional before making any investment decision.

.png)