%20(1).png)

%20(1).png)

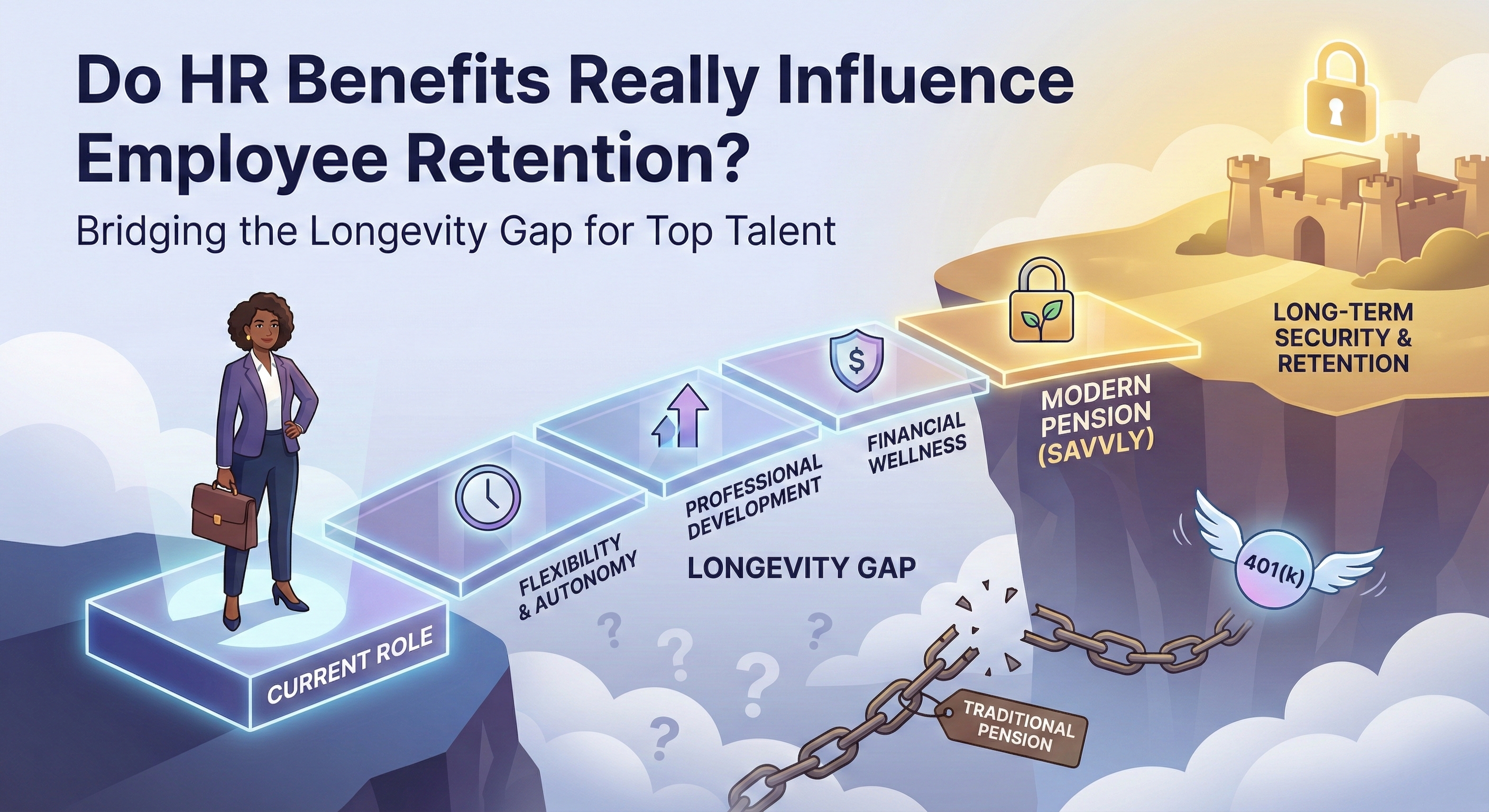

Retirement planning is more manageable than it looks. A few clear steps can put you in a stronger position than most. Experts generally recommend saving 10% to 15% of your income each year, but everyone's retirement needs are different. To help you calculate a more personalized goal, here are four simple steps to follow: estimating your retirement income needs, considering common rules of thumb, using a retirement calculator, and revisiting your plan regularly.

Originally published: September 16, 2024

The first step in determining how much to save for retirement is to estimate your future income needs. Start by considering your current expenses and how they might change in retirement. Think about:

Add these estimates to get a rough idea of your annual expenses in retirement. This figure will serve as a foundation for calculating your savings goal.

There are several rules of thumb that can help simplify retirement planning:

While these rules provide a useful starting point, they should be adjusted based on your individual circumstances and retirement goals.

Retirement calculators are powerful tools that can provide a more personalized savings goal. These calculators typically consider factors such as your current age, income, savings rate, investment returns, and desired retirement age. Many online calculators also allow you to input specific details like expected Social Security benefits, pensions, and other income sources.

Retirement planning isn't a one-time task; it requires ongoing attention. Life events, market conditions, and changes in your financial situation can all impact your retirement plan. Aim to revisit your retirement savings strategy at least once a year or after significant life changes, such as marriage, the birth of a child, a job change, or a major purchase.

During these reviews, update your estimates for expenses, income, and savings, and adjust your plan as needed. Staying proactive and flexible will help you stay on track to meet your retirement goals.

Calculating how much to save for retirement doesn't have to be overwhelming. By estimating your retirement income needs, considering common rules of thumb, using a retirement calculator, and revisiting your plan regularly, you can create a personalized and realistic retirement savings strategy. Starting early and saving consistently can make a significant difference, helping you achieve financial security and peace of mind in your golden years.

The Savvly Longevity Benefit is designed to help investors build potential income at later life milestones. It is not insurance, not a guaranteed product, and not FDIC insured. Learn more at savvly.com/disclosures.

This article is for informational purposes only and does not constitute financial, tax, or investment advice. Consult a qualified financial professional before making retirement planning decisions.

Disclosures

The information on this page is provided for educational purposes only and is not intended as investment, legal, or tax advice. It is designed solely to illustrate how longevity-linked investment benefits may work under certain assumptions. Actual results will vary. All illustrations, examples, and case studies are hypothetical and are intended to demonstrate potential scenarios — not to predict or guarantee actual outcomes. They do not represent the performance of any individual investor, portfolio, or account.

Key Assumptions Used in the Illustrations

Life expectancy and mortality projections are based on the most recent Social Security Administration (SSA) tables available at the time of simulation.

In the event of death or early withdrawal, hypothetical scenarios assume that investors who exit early, or their estate in the event of death, may receive 75% of the lesser of the initial investment or current market value, plus 1% for each full year the account was active. Case studies assume standardized market growth of 8% annually and do not incorporate unexpected market volatility, inflation, changes in interest rates, or changes in an investor's personal circumstances.

Simulations may assume a 3% annual early withdrawal rate prior to payout or death. All figures shown are net of fees. No forecast, projection, or hypothetical return should be relied upon as a promise or representation of future performance.

Past performance is not indicative of future results. The 8% annual market growth rate used in illustrations is a standardized assumption for modeling purposes only and does not represent the historical or expected performance of any specific investment. Note that early or voluntary withdrawals by other participants can affect fund performance and the size of distributions, and that a higher-than-expected number of participants reaching payout milestones may reduce the per-participant benefit received.

Savvly's Longevity Benefit is not a bank product, not FDIC insured, not insured by any federal government agency, not a guaranteed or insured investment, and not insurance. Investment values may decline.

Savvly's Longevity Benefit may not be suitable for all investors. Eligibility to invest is subject to qualification requirements and not all investors will be eligible. Investors should carefully consider their investment objectives, risk tolerance, time horizon, and financial situation before investing. See savvly.com/disclosures for current eligibility criteria, fees, risks, withdrawal terms, and fund assumptions.

This content is published by Savvly, Inc. Savvly has a financial interest in the products described and this content should not be interpreted as independent financial research or analysis. Investors should carefully evaluate their own circumstances and consult a qualified financial professional before making any investment decision.

.png)