Mock-up — For Internal Use Only

Retirement doesn’t stop at 80—neither should your income.

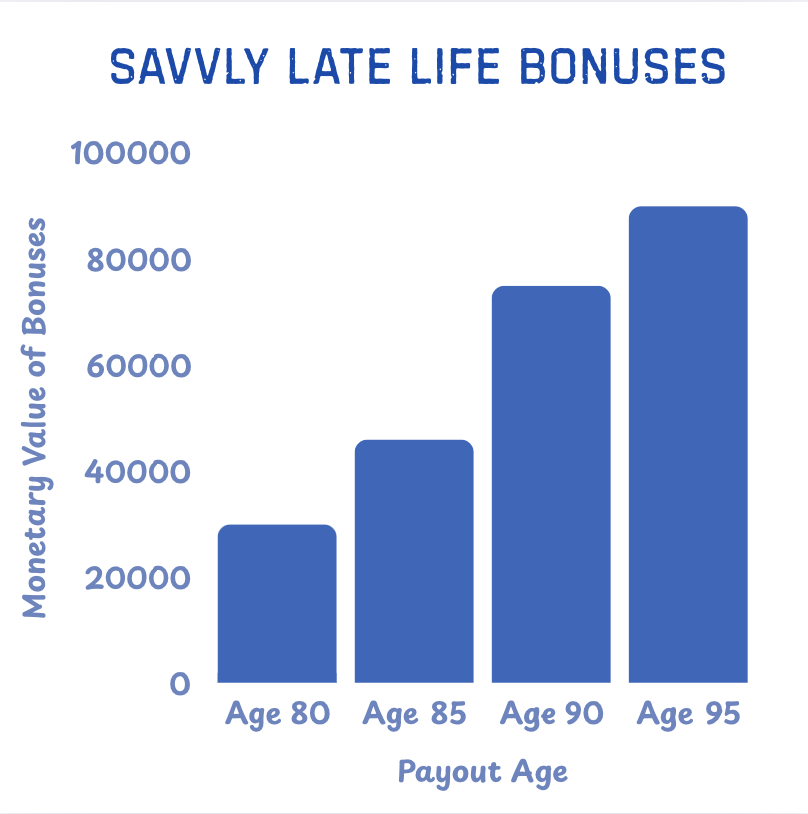

Savvly - A Longevity Hedge to Protect your Retirement

Savvly is a new kind of pooled investment fund that is designed to give additional money later in life—right when you need it most.

Savvly is built on a simple idea: people who live longer should be protected.

Savvly is built on a simple idea: people who live longer should be protected.

.png)

.svg)

.svg)

.png)

.png)

.png)

.svg)

.svg)

.png)